Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Co-Buying a Home Helps with Affordability Today

Buying a home in today’s market can feel like an uphill battle – especially with home prices and mortgage rates putting pressure on your budget. If you’re feeling stuck, co-buying could be one way to help you get your foot in the door. Freddie Mac says:

“If you are an aspiring homeowner, buying a home with your family or friends could be an option.”

But there are some things you’ll want to consider first. Let’s explore why co-buying is gaining popularity right now among some buyers and see if it may make sense for you too.

What Is Co-Buying?

Co-buying means buying a home with someone like a friend, sibling, or even a group of people. And, with today’s high home prices and mortgage rates, it’s an option more people are turning to.

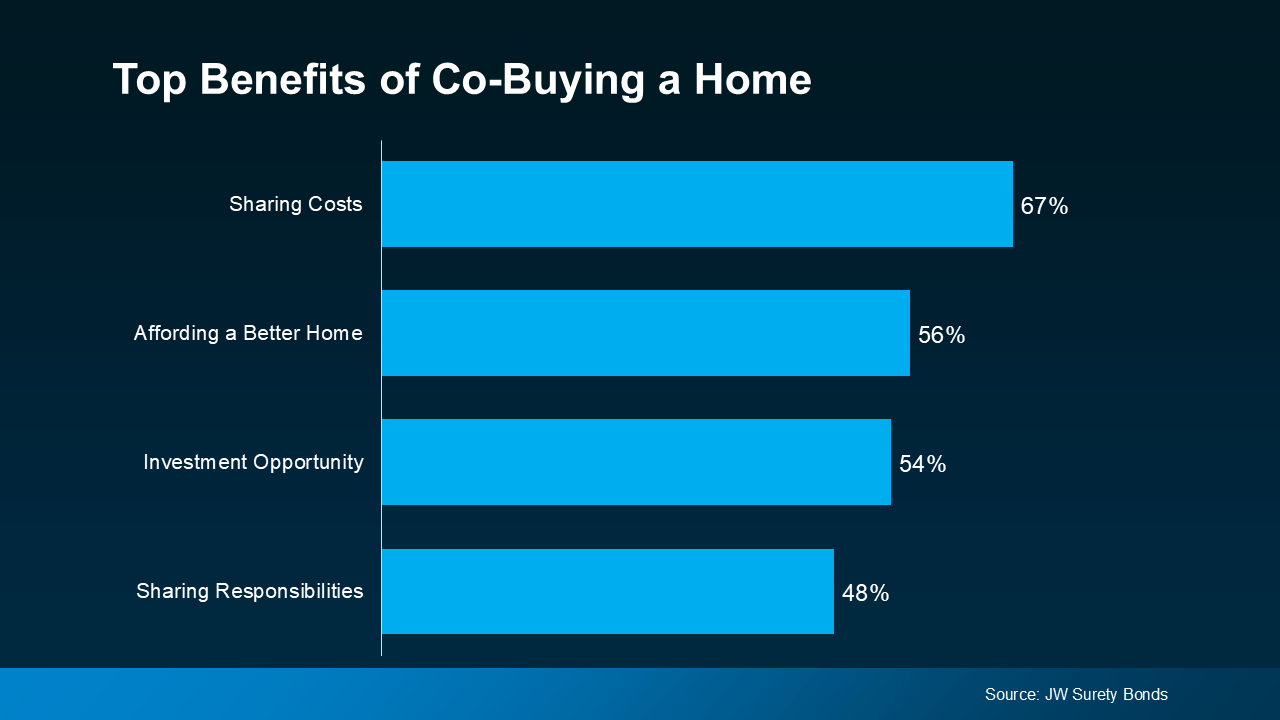

According to a survey done by JW Surety Bonds, nearly 15% of Americans have already co-purchased a home with someone, and another 48% would consider doing it.

Why Consider Co-Buying?

The same survey also asked people about the perks of co-buying a home. Here are some of the top responses (see graph below):

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Affording a Better Home (56%): By pooling your financial resources, you may also be able to afford a larger or higher-quality home than you could have on your own. This may mean getting that extra bedroom, a bigger backyard, or living in a more desirable neighborhood.

Investment Opportunity (54%): Co-buying a home can also be an investment. You could buy a house with someone so you can rent out, which could help generate passive income.

Sharing Responsibilities (48%): Owning a home comes with a lot of responsibilities, including maintenance and upkeep and more. When you co-buy, you share these commitments, which can lighten the load for everyone involved.

Other Co-Buying Considerations

While co-buying has its benefits, there’s something else you need to consider before deciding if this approach is right for you. As Rocket Mortgage says:

“Buying a house with a friend or multiple friends might be a great way for you to achieve homeownership, but it’s not a decision you should make lightly. Before diving in, make sure you understand the financial and logistical hurdles you’ll face, as well as the human and emotional elements that might affect the purchase or, more importantly, your relationship.”

Basically, make sure you and your co-buyer are on the same page about things like how costs will be split, who will handle what responsibilities, and what will happen if one of you wants to sell your share of the home in the future. Leaning on an expert can help you weigh the pros and cons to make that conversation easier.

Bottom Line

If you’re looking to get your foot in the door but are having a tough time with today’s affordability challenges, co-buying could be an option to make your move happen. But, it’s important to plan carefully and make sure all parties are clear on the details. To figure out if co-buying makes sense for you, let’s connect.

Why Now’s Not the Time To Take Your House Off the Market

Has your house been sitting on the market longer than expected? If so, you’re bound to be frustrated by now. Maybe you’re even thinking it’s time to pull the listing and wait to see what 2025 brings. But what you may not realize is, the decision to hold off could actually cost you. Here’s a look at why staying the course could be the smarter move; and Why Now’s Not the Time To Take Your House Off the Market.

Other Sellers Are Pulling Back. Should You Hold Off Too?

According to recent data from Altos Research, the number of withdrawals is increasing – that means more sellers are opting to pull their listings off the market right now. And this isn’t unusual for this time of the year.

In the housing market, there are seasonal ebbs and flows. Inventory levels typically start to drop off a bit headed into the fall season as some sellers delay their plans until the new year. As Mike Simonsen, Founder of Altos Research, explains:

“. . . we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year. In fact, for every two sales, there is another listing withdrawn from the market.”

But is that a smart move? While it might seem like a good idea to pull your listing too, here’s why that approach may not pay off this year.

Today’s Buyers Are Serious and Ready To Act

The biggest reason to stick with your plan to sell now is that the buyers who are looking at this time of year are serious about making a purchase.

They’ve been sitting on the sidelines for a while waiting for affordability to improve. And now that mortgage rates are down from their recent peak, they’re ready to make their move. Mortgage applications are rising – and that’s a leading indicator that buyers are preparing to jump back in. And since they’ve already put their needs on the back burner for so long, they’re even more eager than buyers usually are at this time of year.

These aren’t window shoppers. They’re highly motivated buyers who want to move fast – and that’s the kind of buyer you want to work with. As Freddie Mac says:

“During the fall months, serious homebuyers are eager to settle in to a new home before the holiday season ramps up and the winter weather begins.”

By keeping your home on the market, you increase the chances of attracting people who are truly ready to make a purchase.

Bottom Line

While some sellers are choosing to take their homes off the market, this really isn’t the best move. With serious buyers eager to purchase, this is a great time to sell your house. Let’s connect to make sure we’ve got a strategy in place to make it happen.

Is Your House Priced Too High?

Every seller wants to get their house sold quickly, for as much money as they can, with as few headaches as possible. And chances are, you’re no different.

But did you know one of the biggest things that could jeopardize your success is the asking price for your home? Pricing your house correctly is one of the most crucial steps in the selling process.

So, how do you know if you’re missing the mark? Here are four signs your high asking price might be turning potential buyers away—and why leaning on your real estate agent is the best way to course correct.

1. You’re Not Getting Many Showings or Offers

One of the most obvious signs your house may be overpriced is a lack of showings. If it’s been on the market for several weeks and only a few buyers have come to see it—or worse, you haven’t gotten any offers—it could be a clear indication the price isn’t matching up with what buyers expect. Because buyers who have been looking for a while can easily spot (and write off) a home that seems overpriced.

Your real estate agent will coach you through this, so lean on their experience for what you may want to try to bring more buyers in, including considering a price cut.

2. Buyers Have Consistent Negative Feedback after Showings

And if after the showings you do have, comments from the potential buyers aren’t great, you may need to course correct. Feedback from showings is an important part of understanding how buyers see your house. If they consistently say it’s overpriced compared to other homes they’ve seen, it’s time to reconsider your pricing strategy.

Your agent will gather and analyze this feedback for you, so you can look at how your house stacks up in the market. They can also suggest specific improvements or staging changes to better justify your asking price, or recommend one that aligns with today’s buyer expectations. As the National Association of Realtors (NAR) explains:

“Based on all the data gathered, agents may make adjustments to the initial price recommendation. This could involve adjusting for market conditions, property uniqueness, or other factors that may impact the property’s value.”

3. It’s Been on the Market for Too Long

And that lack of interest is ultimately going to lead to it sitting on the market without any serious bites. The longer it lingers, the more likely it is to raise red flags for buyers, who may wonder if something is wrong with it. Especially in today’s market with growing inventory, a long listing period means your house is stale – and that makes it even harder to sell.

Your real estate agent will be able to give you perspective on how quickly other homes in your area are selling and walk you through what’s working for other sellers. That way you can decide together if there’s something you want to do differently. As a Bankrate article says:

“Check with your agent about the average number of days homes spend on the market in your area. If your listing has been up significantly longer than average, that may be a sign to reduce the price.”

4. Your Neighbor’s House Sold Without an Issue

And here’s the last one to watch out for. If similar homes in your area are selling faster than yours, it’s a clear sign that something is off. This could be due to things like a lack of upgrades, outdated features, or a less desirable location. Or, it may be priced too high.

Your agent will keep you up to date on your competition and what changes, if any, you need to make your home more competitive. They’ll offer advice on small updates that could increase your home’s appeal or how to adjust your strategy to reflect the reality of the market today.

Bottom Line

Pricing a home correctly is both an art and a science. It requires a deep understanding of the market and buyer psychology. And when the price isn’t drawing in buyers, there’s no better resource than your agent on what you may want to do next.

Why Pre-Approval Should Be at the Top of Your Homebuying To-Do List

Since the supply of homes for sale is growing and mortgage rates are coming down, you may be thinking it’s finally your moment to jump into the market. To make sure you’re ready, you need to get pre-approved for a mortgage.

That’s when a lender looks at your finances, including things like your W-2, tax returns, credit score, and bank statements, to figure out what they’re willing to loan you. After that process, you’ll get a pre-approval letter to show what you can borrow. Here are two reasons why this is essential in today’s market.

Pre-Approval Helps You Know Your Numbers

While home affordability is finally starting to show signs of improving, it’s still tight. So, it’s a good idea to talk to a lender about your loan options and how today’s changing mortgage rates will impact your monthly payment. The pre-approval process is the perfect time for that. In addition to determining the maximum amount you can borrow, pre-approval also helps you understand this piece of the puzzle. As Investopedia says:

“Consulting with a lender and obtaining a pre-approval letter allows you to discuss loan options and budgeting with the lender; this step can clarify your total house-hunting budget and the monthly mortgage payment you can afford.”

You should use this information to tailor your home search to what you’re actually comfortable with budget-wise. Since mortgage rates have inched down some lately, you may find you’re able to afford a bit more than you’d expect for your monthly payment, but you still want to avoid overextending. As CNET explains:

“In many cases, a lender may preapprove you for more than you need to spend on a home. And while it can be tempting to look at houses outside your budget, it won’t help you in the long run. Before you start touring homes, figure out how much you can realistically afford and stick to your budget.”

Pre-Approval Makes Your Offer More Appealing

And once you do find a home you want in your budget, pre-approval has another big perk. It not only makes your offer stronger, it also shows sellers you’ve already undergone a credit and financial check. When a seller sees you as a serious buyer, they may be more attracted to your offer because it seems more likely to go through. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

As mortgage rates trend down, more buyers are going to be ready to jump back into the market. And while demand is still limited right now, there’s the potential for competition to pick back up, especially in hot markets. So, why not stack the deck in your favor and make sure you’re putting yourself in the best position possible when you find a home you love?

Bottom Line

If you’re planning on buying a home, don’t forget to get pre-approved early in the process. It can help you get a more in-depth understanding of what you can borrow and shows sellers you mean business.

Falling Mortgage Rates Are Bringing Buyers Back

If you’ve been hesitant to list your house because you’re worried no one’s buying, here’s your sign it may be time to talk with an agent.

After months of high rates keeping buyers on the sidelines, things are starting to shift. Rates are already coming down due to a number of economic factors. And yesterday the Federal Reserve cut the Federal Funds Rate for the first time since they began raising that rate in March 2022. And while they don’t control mortgage rates, this sets the stage for mortgage rates to fall even further than they already have – especially since more cuts from the Fed are expected into next year. And lower mortgage rates are bringing more buyers back into the market. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“A drop in the cost of borrowing will help fuel more homebuyer demand . . . Falling rates will also bring more sellers into the market.”

The best part? You can take advantage of that renewed buyer interest.

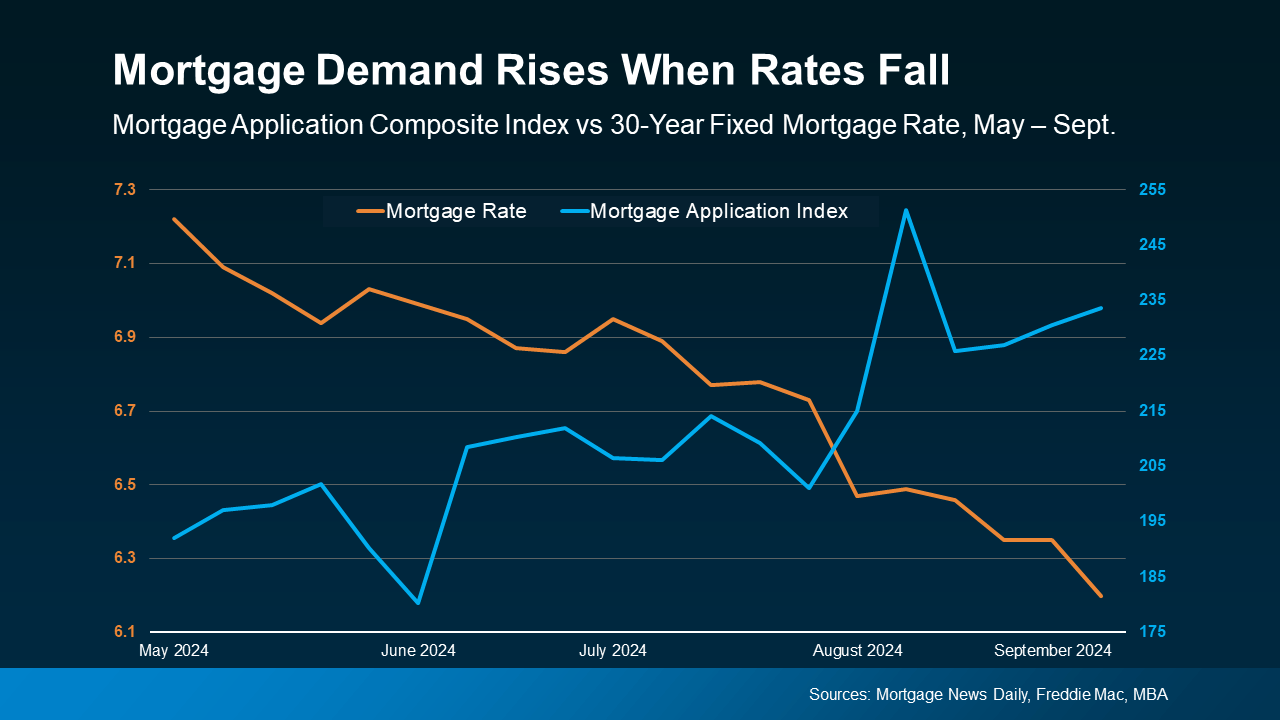

As Rates Fall, Buyer Activity Goes Up

The graph below illustrates the relationship between falling mortgage rates and rising buyer activity. The orange line represents the average 30-year fixed mortgage rate, while the blue line shows the Mortgage Bankers Association (MBA) Mortgage Application Index, which tracks the number of mortgage applications.

As you can see, as mortgage rates (orange) come down, the Mortgage Application Index (blue) rises, showing more people start to re-engage in the process (see graph below):

What This Means for You

What This Means for You

According to the National Association of Realtors (NAR), home sales increased in July, which was a welcome shift after four straight months of declines. If you’re a homeowner thinking about selling, this uptick in buyer activity works in your favor.

More buyers means more competition, which can lead to higher offers and shorter time on the market for your house. And, according to Edward Seiler, AVP of Housing Economics at the Mortgage Bankers Association (MBA), this trend is expected to continue:

“MBA is expecting that slower home-price appreciation, coupled with lower rates, will ease affordability constraints and lead to increased activity in the housing market.”

All in all, the market is becoming more accessible to a wider range of buyers, which could result in even more people looking to purchase a house like yours.

With more buyers entering the market, now’s the time to start getting your house ready to sell.

Bottom Line

The recent decline in mortgage rates is already driving more buyers into the market, and experts project this trend will continue. Let’s work together to take advantage of this increased buyer demand and get your house ready to sell.

The Real Story Behind What’s Happening with Home Prices

If you’re wondering what’s going on with home prices lately, you’re definitely not the only one. With so much information out there, it can be hard to figure out your next move.

As a buyer, you might be worried about paying more than you should. And if you’re thinking of selling, you might be concerned about not getting the price you’re aiming for.

So, here’s a quick breakdown to help clear things up and show you what’s really happening with prices—whether you’re thinking about buying or selling.

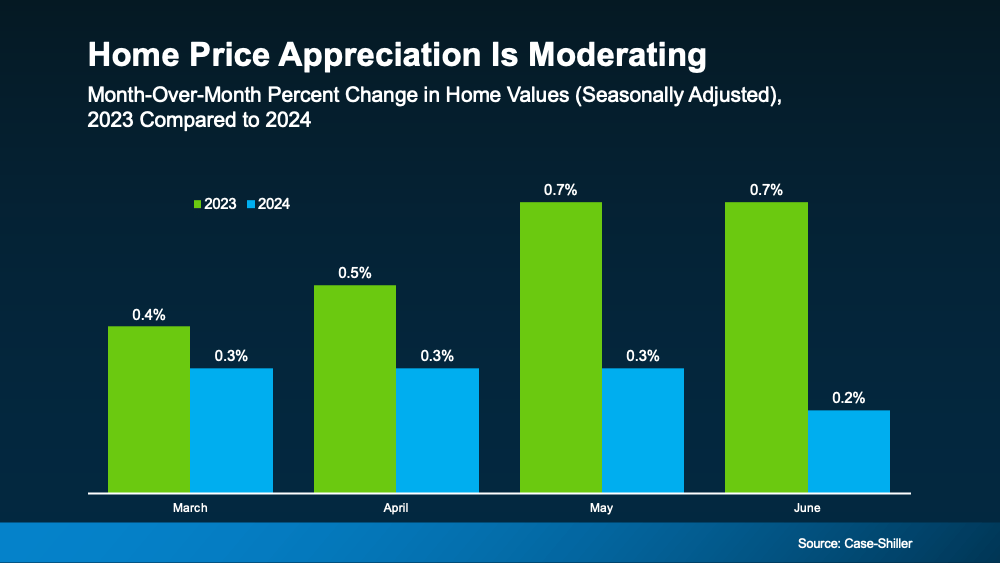

Home Price Growth Is Slowing, but Prices Aren’t Falling Nationally

Throughout the country, home price appreciation is moderating. What that means is, prices are still going up, but they’re not rising as quickly as they were in recent years. The graph below uses data from Case-Shiller to make the shift from 2023 to 2024 clear:

But rest assured, this doesn’t mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they’re not climbing as fast as they were when they skyrocketed just a few years ago.

What’s Next for Home Prices? It’s All About Supply and Demand

You might be curious where prices will go from here. The answer depends on supply and demand, and it’s going to vary by local market.

Nationally, the number of homes for sale is going up, but there still aren’t enough of them to meet today’s buyer demand. That’s keeping upward pressure on prices – even though recent inventory growth has caused that home price appreciation to slow. Danielle Hale, Chief Economist at Realtor.com, said:

“. . . today’s low but quickly improving for-sale inventory has ushered in more market balance than would otherwise be expected . . . This should help home prices maintain a slower pace of growth.”

And here’s one other thing you may not have considered that could play a role in where prices go from here. Since experts say mortgage rates should continue to decline, it’s likely more buyers will re-enter the market in the months ahead. If demand picks back up, that could make prices climb a bit further.

Why You Should Work with a Local Real Estate Agent

While national trends give a big-picture view, real estate is always local – especially when it comes to prices. What’s happening in your neighborhood might be different from the national average based on what supply and demand look like in your market. That’s why it’s crucial to get local insights from a knowledgeable real estate agent.

As your go-to source for everything related to home prices, a local agent can provide the most current data and trends specific to your area.

So, if you’re planning to sell, they can help you price your house accurately. And when you’re ready to buy, they can find the right home that fits your budget and your needs.

Bottom Line

Home prices are still rising, just not as quickly as before. Whether you’re thinking about buying, selling, or just curious about what your house is worth, let’s connect so you have the personalized guidance you need.

How the Federal Reserve’s Next Move Could Impact the Housing Market

Now that it’s September, all eyes are on the Federal Reserve (the Fed). The overwhelming expectation is that they’ll cut the Federal Funds Rate at their upcoming meeting, driven primarily by recent signs that inflation is cooling, and the job market is slowing down. Mark Zandi, Chief Economist at Moody’s Analytics, said:

“They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

But what does this mean for the housing market, and more importantly, for you as a potential homebuyer or seller?

Why a Federal Funds Rate Cut Matters

The Federal Funds Rate is one of the key factors that influences mortgage rates – things like the economy, geopolitical uncertainty, and more also have an impact.

When the Fed cuts the Federal Funds Rate, it signals what’s happening in the broader economy, and mortgage rates tend to respond. While a single rate cut might not lead to a dramatic drop in mortgage rates, it could contribute to the gradual decline that’s already happening.

As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), points out:

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

And any upcoming Federal Funds Rate cut likely won’t be a one-time event. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

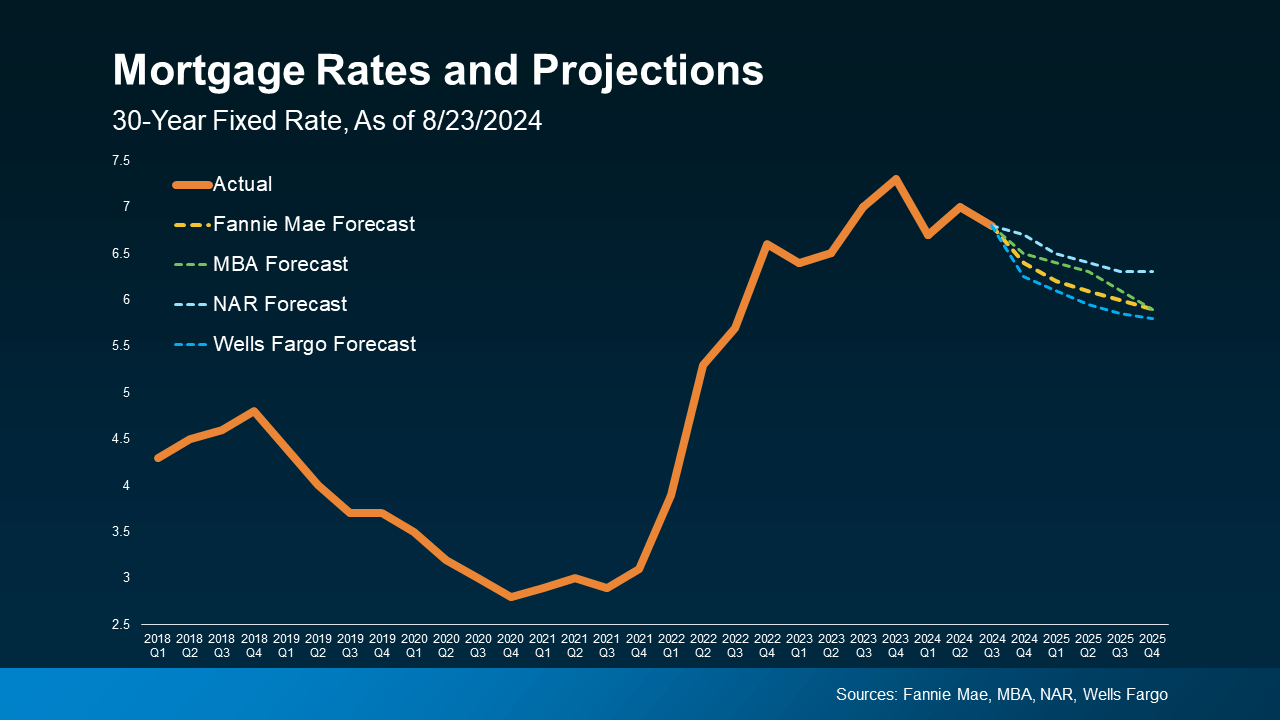

The Projected Impact on Mortgage Rates

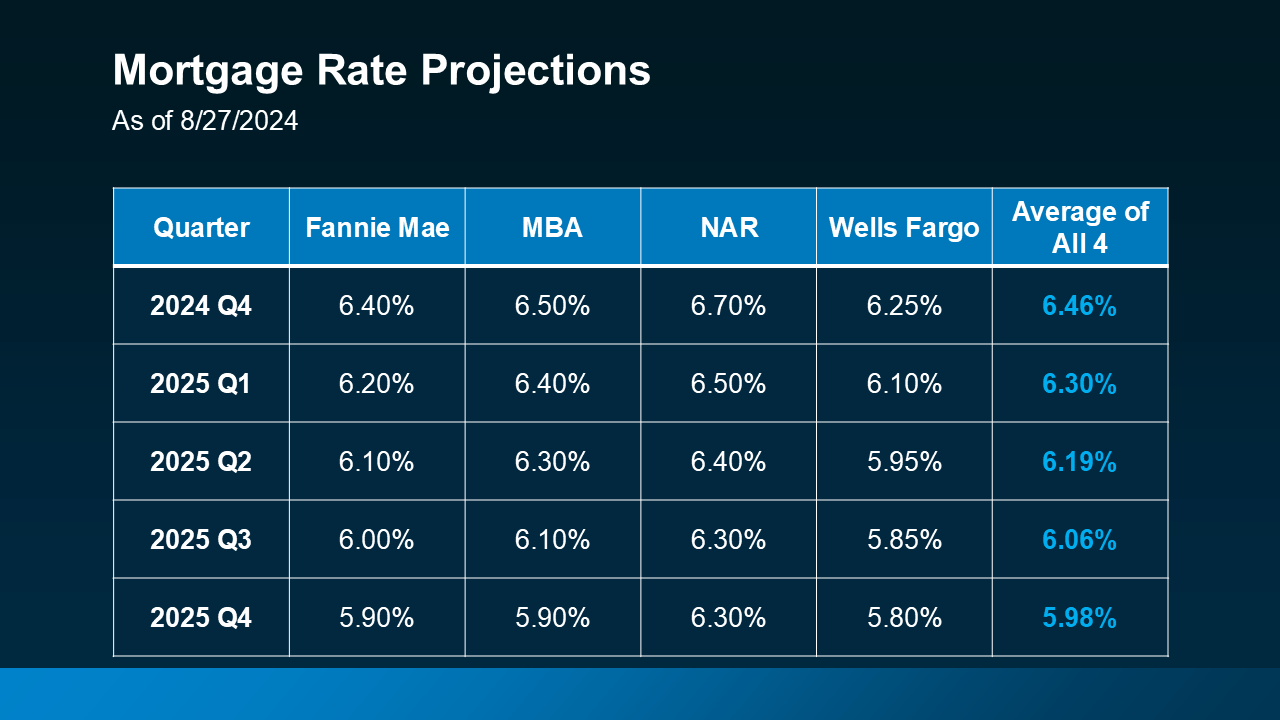

Here’s what experts in the industry project for mortgage rates through 2025. One contributing factor to this ongoing gradual decline is the anticipated cuts from the Fed. The graph below shows the latest forecasts from Fannie Mae, MBA, NAR, and Wells Fargo (see graph below):

So, with recent improvements in inflation and signs of a cooling job market, a Federal Funds Rate cut is likely to lead to a moderate decline in mortgage rates (shown in the dotted lines). Here are two big reasons why that’s good news for both buyers and sellers:

So, with recent improvements in inflation and signs of a cooling job market, a Federal Funds Rate cut is likely to lead to a moderate decline in mortgage rates (shown in the dotted lines). Here are two big reasons why that’s good news for both buyers and sellers:

1. It Helps Alleviate the Lock-In Effect

For current homeowners, lower mortgage rates could help ease the lock-in effect. That’s where people feel stuck within their current home because today’s rates are higher than what they locked in when they bought their current house.

If the fear of losing your low-rate mortgage and facing higher costs has kept you out of the market, a slight reduction in rates could make selling a bit more attractive again. However, this isn’t expected to bring a flood of sellers to the market, as many homeowners may still be cautious about giving up their existing mortgage rate.

2. It Should Boost Buyer Activity

For potential homebuyers, any drop in mortgage rates will provide a more inviting housing market. Lower mortgage rates can reduce the overall cost of homeownership, making it more feasible for you if you’ve been waiting to make a move.

What Should You Do?

While a Federal Funds Rate cut is not expected to lead to drastically lower mortgage rates, it will likely contribute to the gradual decrease that’s already happening.

And while the anticipated rate cut represents a positive shift for the future of the housing market, it’s important to consider your options right now. Jacob Channel, Senior Economist at LendingTree, sums it up well:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

Bottom Line

The expected Federal Funds Rate cut, driven by improving inflation and slower job growth, is likely to have a positive, though gradual, impact on mortgage rates. That could help unlock opportunities for you. When you’re ready, let’s connect. That way you’ll be prepared to take action when the time is right for you.

2025 Housing Market Forecasts: What To Expect

Looking ahead to 2025, it’s important to know what experts are projecting for the housing market. And whether you’re thinking of buying or selling a home next year, having a clear picture of what they’re calling for can help you make the best possible decision for your homeownership plans.

Here’s an early look at the most recent projections on mortgage rates, home sales, and prices for 2025.

Mortgage Rates Are Projected To Come Down Slightly

Mortgage rates play a significant role in the housing market. The forecasts for 2025 from Fannie Mae, the Mortgage Bankers Association (MBA), the National Association of Realtors (NAR), and Wells Fargo show an expected gradual decline in mortgage rates over the course of the next year (see chart below):

Mortgage rates are projected to come down because continued easing of inflation and a slight rise in unemployment rates are key signs of a strong but slowing economy. And many experts believe these signs will encourage the Federal Reserve to lower the Federal Funds Rate, which tends to lead to lower mortgage rates. As Morgan Stanley says:

“With the U.S. Federal Reserve widely expected to begin cutting its benchmark interest rate in 2024, mortgage rates could drop as well—at least slightly.”

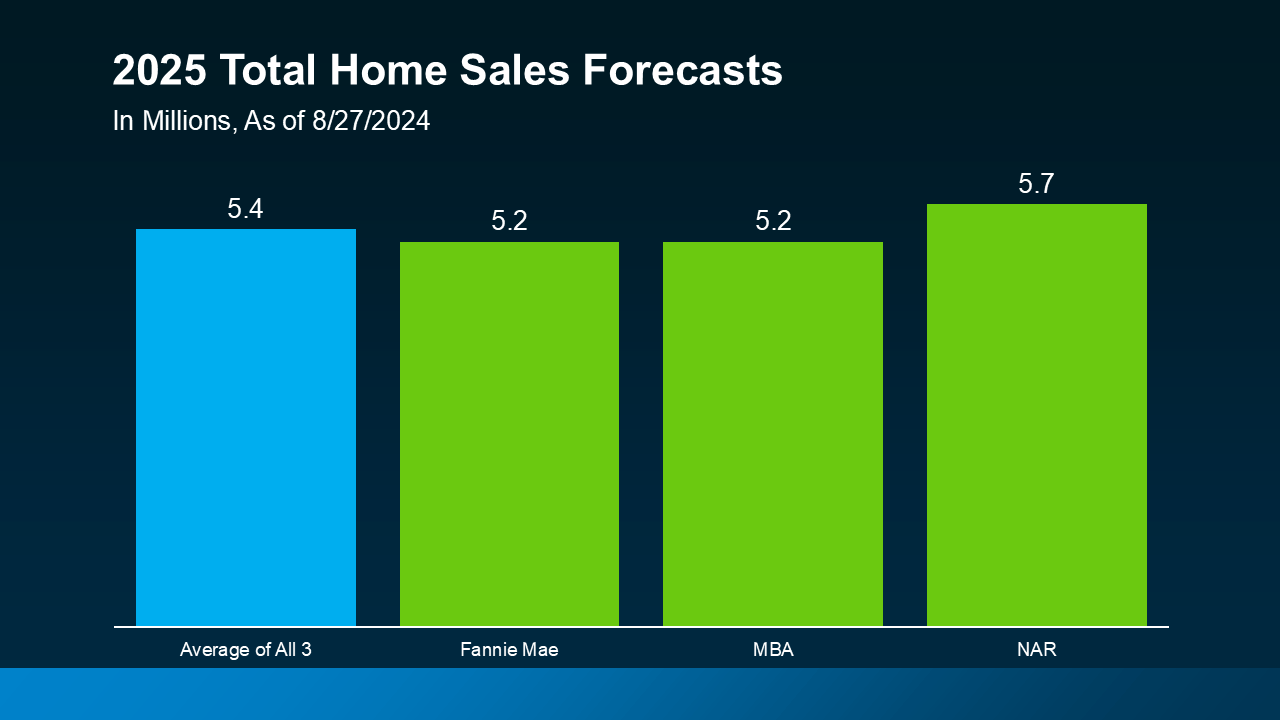

Expect More Homes To Sell

The market will see an increase in both the supply of available homes on the market, as well as a rise in demand, as more buyers and sellers who have been sitting on the sidelines because of higher rates choose to make a move. That’s one big reason why experts are projecting an increase in home sales next year.

According to Fannie Mae, MBA, and NAR, total home sales are forecast to climb slightly, with an average of about 5.4 million homes expected to sell in 2025 (see graph below):

That would represent a modest uptick from the lower sales numbers in 2023 and 2024. For reference, about 4.8 million total homes were sold in 2023, and expectations are for around 4.5 million homes to sell this year.

While slightly lower mortgage rates are not expected to bring a flood of buyers and sellers back to the market, they certainly will get more people moving. That means more homes available for sale – and competition among buyers who want to purchase them.

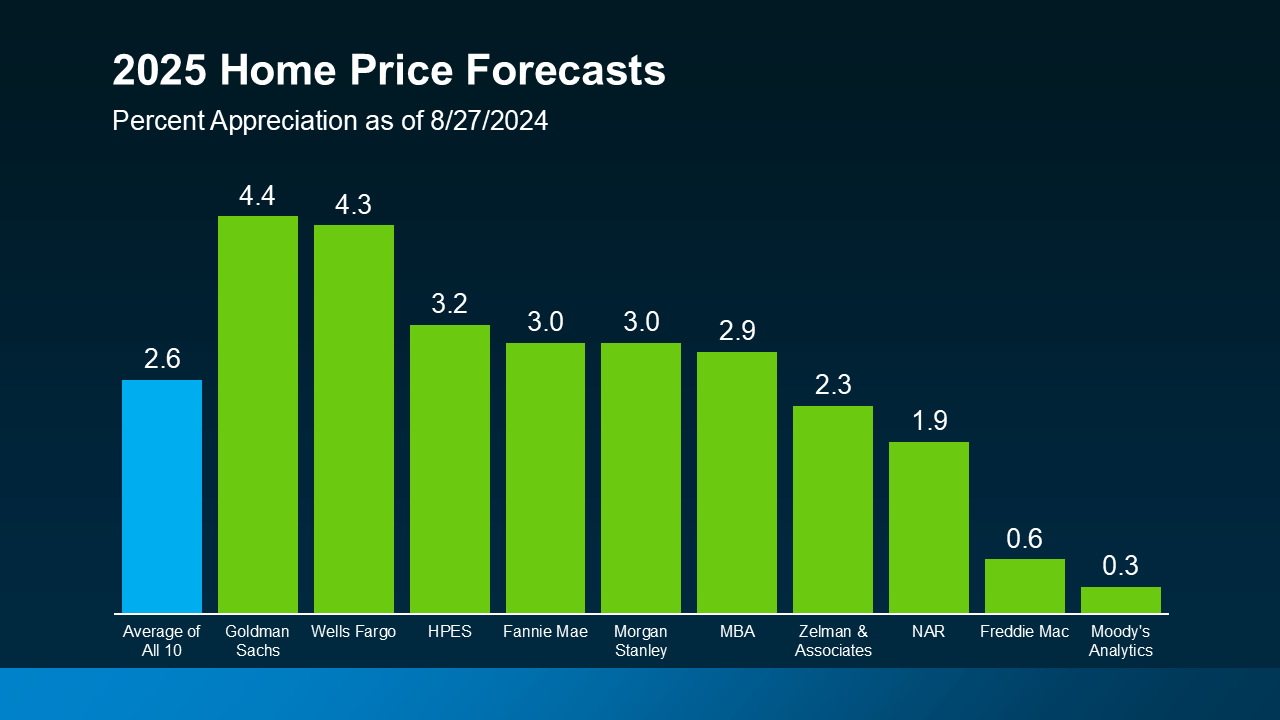

Home Prices Will Go Up Moderately

More buyers ready to jump into the market will put continued upward pressure on prices. Take a look at the latest price forecasts from 10 of the most trusted sources in real estate (see graph below):

On average, experts forecast home prices will rise nationally by about 2.6% next year. But as you can see, there’s a range of opinions on how much prices will climb. Experts agree, however, that home prices will continue to increase moderately next year at a slower, more normal rate. But keep in mind, prices will always vary by local market.

Bottom Line

Understanding 2025 housing market forecasts can help you plan your next move. Whether you’re buying or selling, staying informed about these trends will ensure you make the best decision possible. Let’s connect to discuss how these forecasts could impact your plans.

NAR Settlement, Market Shifts, AI, and High-Interest Rates

![]()

The real estate landscape is undergoing significant transformations. Traditional practices are being revisited, market dynamics are shifting, and innovative technologies are making their mark. This article explores four major influences currently redefining the real estate sector: the recent National Association of Realtors (NAR) settlement, changes in market conditions, the impact of rising interest rates, and the integration of Artificial Intelligence (AI).

NAR Settlement: Changing Commission Structures

In a landmark decision in March 2024, the National Association of Realtors (NAR) resolved a lawsuit that challenged its long-held commission practices, where a typical 5-6% commission was shared between the seller’s and buyer’s agents. This settlement has reduced NAR’s dominance over commission setups.

Potential Impact

This development could usher in a wave of competition among real estate agents as alternative pricing models, such as flat fees or hourly rates, become more prevalent. This shift offers buyers more freedom in choosing their agents without the burden of a standard commission impacting their budget.

Market Dynamics: From Booming to Shifting

After years of a robust real estate market, signs of a shift are becoming evident, indicating a move from a booming market to one in flux.

Impact on the Settlement

The ramifications of the NAR settlement may become more noticeable in a cooling market. Sellers seeking to maximize their returns might lean towards agents who offer more competitive commission structures to remain attractive.

The Effect of High-Interest Rates: Cooling Demand

As interest rates climb, obtaining mortgages becomes pricier, which might deter prospective buyers and place downward pressure on property prices.

Increased Competition

With fewer buyers in the market, real estate agents might face stiffer competition for listings. This could drive agents to embrace new technologies, such as AI, or to enhance their service offerings to stand out in the market.

AI’s Role in Real Estate: Enhancing Efficiency and Customization

Artificial Intelligence is steadily making inroads into the real estate industry, promising to revolutionize it with enhanced efficiency and tailored services.

Potential Applications

AI tools are capable of aiding in property valuation, performing market analyses, generating leads, and even designing virtual property tours.

Impact on Agents

While AI is not expected to completely replace human agents soon, it can streamline routine tasks, allowing agents to dedicate more time to personalizing client interactions and strengthening relationships.

The real estate sector is navigating through a complex terrain. The NAR settlement is fostering greater competition, while evolving market conditions and rising interest rates introduce new challenges. AI technologies offer the potential to boost efficiency and transform agent operations. The unfolding of these trends will significantly shape the future of the real estate industry.

Home Prices and Mortgage Rates?

What’s Next for Home Prices and Mortgage Rates?

Navigating the housing market can feel overwhelming, especially with the constant changes in home prices and mortgage rates. Whether you’re a first-time homebuyer, a homeowner thinking about upgrading, or someone considering selling, understanding what influences these key factors is crucial. In this article, we’ll explore the current state of the housing market, examine the factors that affect home prices and mortgage rates, and offer insights into what the future might hold.

Current State of the Housing Market

Overview of Recent Trends

The housing market has experienced significant shifts over the past few years, largely due to the COVID-19 pandemic. Initially, home prices surged as demand far outpaced supply, driven by historically low mortgage rates and the desire for more space. However, as we enter 2024, the dynamics of the market are starting to change.

Impact of the Pandemic on Home Prices

The pandemic introduced a unique set of challenges and opportunities for the housing market. At first, there was a rush to buy homes, spurred by low mortgage rates and the need for home offices. This surge in demand pushed home prices to record highs. Now, as the economy stabilizes, we are beginning to see a normalization in home price growth.

Factors Influencing Home Prices

Economic Indicators

Economic health is a major driver of home prices. Factors such as inflation, employment levels, and GDP growth play significant roles in shaping the market.

- Inflation Rates

Inflation affects everything from the cost of groceries to the price of homes. When inflation rises, the purchasing power of money decreases, often leading to higher home prices as sellers aim to maintain their profit margins. - Employment Rates

A strong employment market means more people have the financial stability to buy homes, which increases demand and drives up prices. Conversely, high unemployment can suppress demand, potentially stabilizing or even lowering home prices. - GDP Growth

The Gross Domestic Product (GDP) is a measure of overall economic activity. Typically, strong GDP growth correlates with a healthy housing market, as economic prosperity encourages more home buying.

Supply and Demand Dynamics

The balance between housing supply and demand is another critical factor in determining home prices.

- Housing Supply Shortages

A shortage of available homes can drive prices up as buyers compete for limited inventory. This shortage can result from various factors, including zoning laws, construction delays, and natural disasters. - Population Growth and Housing Demand

Areas experiencing rapid population growth often see increased demand for housing. As more people move into these regions, competition for homes intensifies, pushing prices higher. - Building Permits and New Construction

The rate at which new homes are built also affects supply. An increase in building permits and new construction can help alleviate supply shortages and moderate price growth.

Interest Rates and Mortgage Rates

Current Mortgage Rates

Mortgage rates directly impact home affordability. Over the past year, rates have fluctuated, influenced by Federal Reserve policies and broader economic conditions.

Historical Trends in Interest Rates

Looking at historical trends can provide context for current rates. Historically, mortgage rates have varied widely, influenced by factors like inflation, economic policies, and global financial events.

Federal Reserve Policies

The Federal Reserve’s monetary policies, including interest rate adjustments, play a crucial role in determining mortgage rates. Typically, when the Fed raises interest rates to combat inflation, mortgage rates follow suit.

Predictions for Home Prices

Expert Opinions on Future Home Prices

Experts have differing opinions on the future of home prices. Some predict continued growth, although at a slower pace, while others foresee a slight correction as the market balances itself.

Regional Variations in Home Price Predictions

Home price trends can vary significantly by region. Areas with strong economic growth and high demand may continue to see price increases, while others might experience stabilization or slight declines.

Predictions for Mortgage Rates

Forecasts from Financial Institutions

Financial institutions offer various forecasts for future mortgage rates. Most agree that rates will likely rise modestly as the economy continues to recover.

Factors Affecting Future Mortgage Rates

Several factors will influence future mortgage rates, including inflation, Federal Reserve policies, and the overall economic outlook.

Impact on Homebuyers and Sellers

Advice for First-Time Homebuyers

First-time homebuyers should focus on financial preparedness, understanding market conditions, and working with experienced real estate agents to navigate the complexities of the market.

Strategies for Current Homeowners

Current homeowners considering selling should stay informed about market trends, invest in home improvements, and work with professionals to maximize their home’s value.

Tips for Navigating the Market

Understanding Market Trends

Staying informed about market trends is crucial. Regularly reading market reports and news can provide valuable insights into the best times to buy or sell.

Working with Real Estate Agents

A knowledgeable real estate agent can be an invaluable asset. They can provide expert advice, market insights, and negotiation support to help you achieve your real estate goals.

Mortgage Options and Financial Planning

Understanding your mortgage options and having a solid financial plan are essential. Explore different loan types, interest rates, and repayment plans to find the best fit for your situation.

The Role of Government Policies

Housing Policies and Regulations

Government policies and regulations can significantly impact the housing market. Policies aimed at increasing housing supply, providing buyer assistance, and regulating mortgage lending all play a role.

Government Programs and Assistance

Various government programs are available to assist homebuyers, particularly first-time buyers. These programs can provide financial assistance, lower interest rates, and other benefits.

Conclusion

In conclusion, the future of home prices and mortgage rates is shaped by a complex interplay of economic indicators, supply and demand dynamics, and government policies. While predicting exact trends can be challenging, staying informed and working with professionals can help you navigate the market successfully.

Resource Links

Federal Reserve Economic Data (FRED)

National Association of Realtors (NAR) – Research & Statistics

Zillow Research

Mortgage Bankers Association (MBA) – Research & Forecasts

U.S. Census Bureau – Housing Data